PCAF-Aligned Avoided Emissions

Prove What Your

Green Finance Achieves.

PCAF's December 2025 guidance requires avoided emissions to be calculated separately from your GHG inventory. VeriFund enforces this by architecture. Operating on governed disclosure data, same attribution methodology, mandatory separation, audit-grade evidence.

The Credibility Gap

Where Avoided Emissions

Claims Break Down.

Green capital does not fail because assets underperform. It fails because avoided emissions claims cannot be defended. Across African markets, impact claims collapse under review for the same three reasons.

The Baseline Problem

No Credible Counterfactual

Baselines are invented after the fact, adjusted between periods, or chosen to maximize impact claims.

Result: Greenwashing Accusations.

The Attribution Problem

Inconsistent Methodology

Avoided emissions use different attribution than financed emissions. Auditors notice. Credit committees reject.

Result: Methodological Doubt.

The Aggregation Problem

Netting Against GHG Inventory

Avoided emissions are subtracted from financed emissions to claim "net positive" portfolios. PCAF explicitly prohibits this.

Result: Regulatory Rejection.

This is not a data problem. It's an avoided emissions calculation problem.

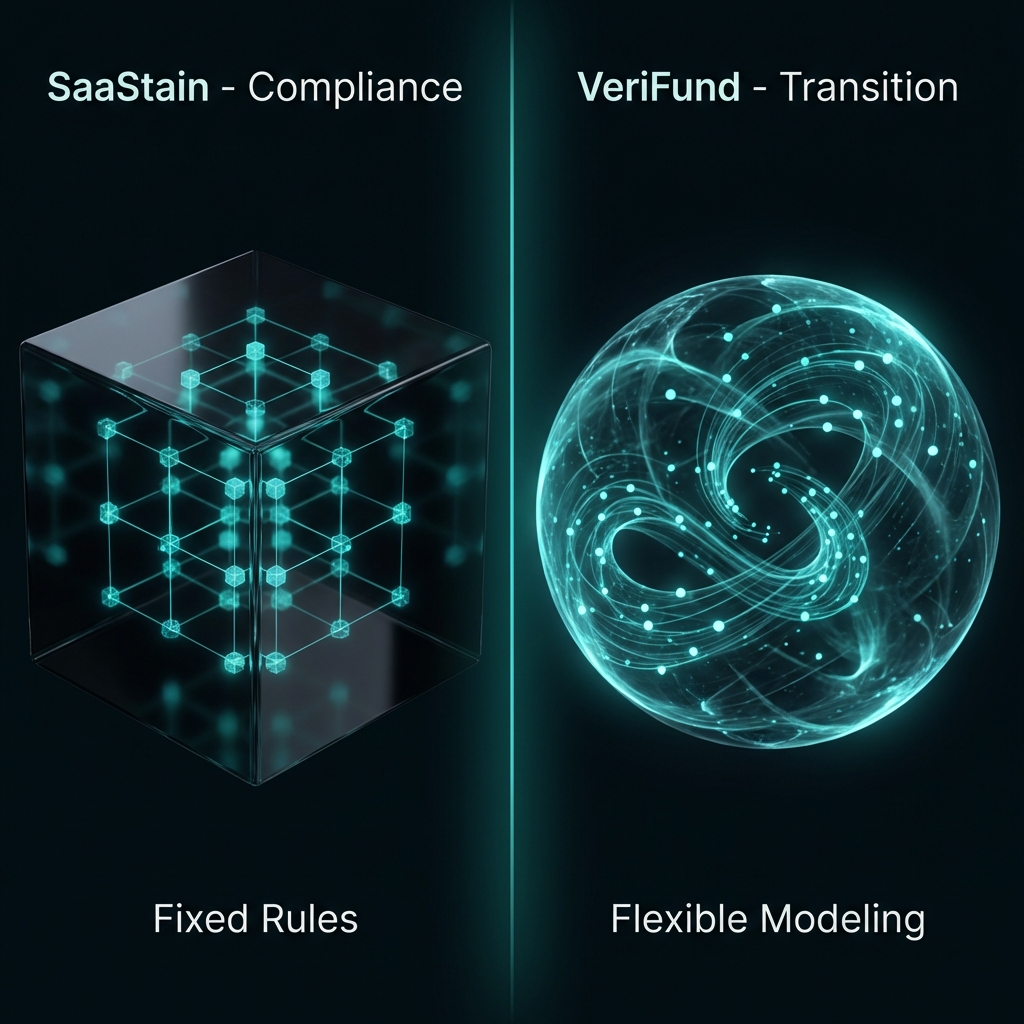

The PCAF Separation Rule

Two Ledgers. One Asset.

Never Aggregated.

PCAF's December 2025 guidance is explicit: avoided emissions and financed emissions are separate metrics with separate purposes. VeriFund enforces this by architecture.

SaaStain: Financed Emissions

"What emissions does the bank's financing create?"

PCAF Part A. Reported in GHG Inventory (Scope 3 Category 15). Measures climate risk exposure.

VeriFund: Avoided Emissions

"What emissions does the green project prevent?"

PCAF Supplemental Guidance. Reported separately from GHG Inventory. Measures climate solution impact.

The PCAF Rule: "Avoided emissions shall not be aggregated for portfolio-level comparisons and shall not be used to substantiate net-zero claims."

VeriFund enforces this by architecture. The two ledgers share asset identity - never calculations. Any attempt to net, restate, or aggregate these metrics is structurally blocked by the system.

What VeriFund Does

Avoided Emissions Calculation.

Asset by Asset.

VeriFund calculates avoided emissions per PCAF guidance - baseline locked at origination, performance measured continuously, evidence generated for every calculation.

Performance Data Ingestion

Telemetry, usage logs, fuel consumption. Direct from source, not reconstructed from surveys.

Baseline Lock (Counterfactual)

The "what would have happened" scenario is declared and locked before tracking begins. No retroactive adjustments.

Avoided Emissions Calculation

Baseline minus solution, calculated continuously. Not reconstructed annually from spreadsheets.

Methodology Versioning

Every factor, formula, and assumption change is versioned, timestamped, and signed. Audit trail is automatic.

The rule: If the baseline changes, it's a new calculation - not an edit.

Solutions and enablers reported separately per PCAF guidance.

How It Works

From Green Asset to

Evidence Object.

Register (Asset Identity)

Green asset registered with financing metadata. Linked to SaaStain by asset ID - but calculations remain separate.

Declare (Baseline Lock)

Counterfactual scenario defined, approved by named signer, and locked before tracking begins. This is the "what would have happened" benchmark.

Monitor (Performance Ingestion)

Operational data flows in. Avoided emissions calculated against locked baseline. Data gaps flagged with quality scores, not estimated.

Generate (Evidence Object)

Tamper-evident record with inputs, baseline, solution, formula, outputs, data quality score, and cryptographic signature. This is your audit artifact.

The evidence object is the disclosure.

Green Asset Coverage

Different Assets. Same Methodology.

Avoided emissions calculation adapts to asset physics. Governance remains rigid.

Infrastructure Dualism

Two Disclosures. One Infrastructure.

Same governance. Reported separately.

SaaStain produces the governed inventory. VeriFund consumes it to calculate avoided emissions. Same attribution method, same audit trail, never netted.

Explore SaaStain Calculate Avoided Emissions.

Correctly.

One period.

PCAF GUIDANCE IS LIVE

Green bond investors expect avoided emissions data. Regulators expect PCAF compliance. Be the bank that has both.

Consultative, not transactional. No commitment beyond the conversation.

See the Calculation